Municipals were steady on Monday as New York City took orders of over $110 million on the first day of a two-day retail order period for $1.039 billion of general obligation bonds. Investors prepared for a week that will see nearly $10 billion of new volume come to market.

Triple-A benchmark bonds from 2022 to 2025 were unchanged, according to Refinitiv Municipal Market Data. Meanwhile, the benchmark 10-year and 30-year Treasury yield closed at 1.255% and 1.924%, respectively. Municipal to U.S. Treasury ratios were at 70% in 10 years and 78% in 30 years.

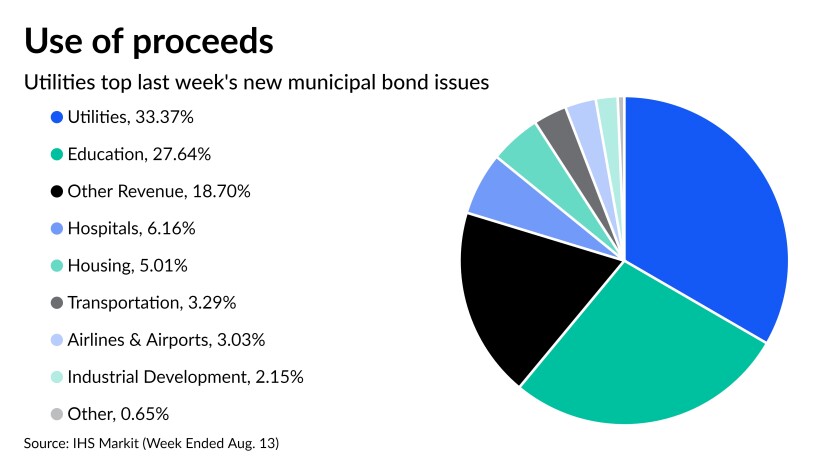

Utilities saw the top use of proceeds from the municipal bonds that were sold last week, according to IHS Markit It was followed by education and other types of revenue bonds.

“It’s been really lethargic in the last few weeks, with a drift in the long end of the market, but today you have a 10-year [Treasury yield] back to a 1.25% from as cheap as 1.36%,” a New York manager said Monday morning.

He called the first day of the NYC retail order period a “good start” on a sleepy summer Monday that was “right on track” for retail investors, many of whom have had some sticker shock at the current municipal rates.

The deal is part of the $9.76 billion on tap in the primary market this week, largely dominated by New York paper.

The NYC deal (Aa2/AA/AA-/AA+), which will be priced for institutions on Wednesday, includes $950 million of fiscal 2022 Series A, serials 2023-2025, 2031-2050 and $89.325 million of reoffering exempts, 2026-2

030. Citigroup Global Markets is the book running syndicate manager.

New York City is also set to competitively sell $250 million of taxable GOs at 10:45 a.m., ET, Wednesday.

The manager said the market was steady, but tentative Monday, with strong demand expected for the NYC GOs, as well as for the New York Liberty Development Corp. (/A/A-/) sale of $1.225 billion of 4 World Trade Center Project tax-exempt liberty revenue refunding green bonds on Wednesday. Goldman Sachs is the senior book-runner.

Cash-flush investors should be eager to take advantage of the flurry of supply as summer nears end, the manager said — if they can swallow the current lackluster yield levels.

All substantially sized deals have done well lately as there is a lot of money circling in the market in August, he noted.

But, at the same time, he said the market technicals aren’t as attractive as investors would like.

“It’s difficult for retail at these rates, and it’s even difficult for some institutions at these percentages,” he explained.

For example, municipals in five years are yielding 48% of the comparable Treasury yield, which he said is “not overly attractive.”

Sweet Big Apple deal

Investors showed their interest in fresh New York paper as the city launched the first of its two-day retail order period — on the heels of a positive outlook change by Fitch Ratings on Friday.

Fitch moved up the city’s GO outlook to stable from negative ahead of its sale, which should add to its already strong appeal with investors, according to the New York manager.

With over $110 million spoken for as of close of trading Monday, the retail order period continues on Tuesday.

The outlook upgrade “definitely helped” and follows in line with a trend of positive outlook revisions by rating agencies lately in an adjustment period as the second year of the COVID-19 pandemic progresses, he said.

He said he didn’t expect the city’s deal to be affected by the growing concern over the Delta variant — even though the deal is being priced the same week as the city begins requiring proof of COVID-19 vaccinations to use public places, such as indoor dining, gyms, sports venues, and museums.

“With the care package the government is committed to helping everyone — and that helps creditwise and makes people more comfortable,” he said.

Tapering

As the markets remain focused on when the Federal Reserve decides to taper asset purchases, one analyst says liftoff will be more dramatic for the markets.

“The announcement of tapering is unlikely to create a large shock in the market, though the U.S. Treasury curve should eventually steepen again,” said Sebastien Galy, senior macro strategist at Nordea Asset Management. “The market simply had a long time to prepare for tapering. The real shock will come when the debate on a cycle of Fed rate hike starts.”

While many thought next week’s Jackson Hole symposium would shed more light on tapering, that is no longer the case, as the spread of the Delta variant of COVID-19 combined with the high number of unemployed keeps the Fed in a wait-and-see mode.

“The reason the market is so concerned about the Federal Reserve tapering its bond purchases is that it could start to reverse the many gains of quantitative easing at a time when many assets are expensive and leverage elevated,” Galy said. “The example of the temper tantrum in 2013 is also disconcerting, but the reality now is more complex.”

While tapering could curb growth, he said, “the real problem for growth and any highly leveraged and expensive asset class is when Fed expectations of raising rates start to significantly ramp-up,” which is expected next year.

And while much of the inflationary pressures should prove transitory, Galy added, “wages and rents are likely to be a persistent pressure.”

December seems to be the new expectation for a taper announcement, according to Morgan Stanley.

“Rising concerns over the Delta variant and increased angst around inflation are not enough to slow the Fed’s march toward tapering,” Ellen Zentner, Morgan Stanley Chief U.S. Economist, wrote in a note. Labor market gains, “updated forecasts, and nascent signs of cooling inflation, we think, keep the FOMC on track to announce the taper at its December meeting.”

But, others think taper hints will come next week. “With mounting evidence of sustained robust activity … at the upcoming symposium in Jackson Hole, Chairman [Jerome] Powell will likely be compelled to drop a stronger hint, if not outright specify, that tapering is on the way,” said Stifel Chief Economist Lindsey Piegza

Meanwhile, Cato Senior Fellow and Director of the Center for Monetary and Financial Alternatives George Selgin applauded those fed president ready to start tapering. “Those purchases have outlived their purpose of stimulating employment and supporting prices during the COVID-19 crisis,” he said. “Moreover, it makes little sense for the Fed to continue creating bank reserves at the present rate while simultaneously reducing them through its overnight reverse-repo program, where over $1 trillion in former reserve balances — roughly half of those created by the Fed’s COVID-19 purchases — are now parked.”

And with the Fed having just established a standing repo facility, Selgin said, it’s “unlikely that even relatively aggressive tapering will result in a ‘taper tantrum’ of the sort that erupted back in 2013.”

Friday’s July employment report and the June JOLTs report “clearly suggest that the Fed’s criteria of ‘substantial further progress’ has been achieved and is no longer ‘a ways off,’” said Berenberg chief economist for the U.S., Americas and Asia Mickey Levy.

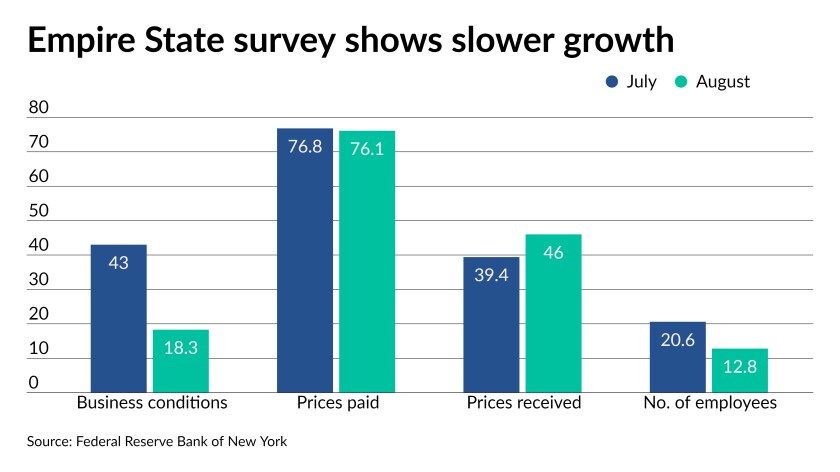

The only indicator released on Monday, the Empire State Manufacturing Survey, suggested slowing growth in the region, as the general business conditions index plunged to 18.3 in August from 43.0 in July.

New orders also dropped, to 14.8 from 33.2, while prices paid dipped to 76.1 from 76.8, prices received climbed to 46.0 from 39.4, and the number of employees index fell to 12.8 from 20.6. But the future business conditions index rose to 46.5 in August from 39.5 in July.

Summer strength ahead of potential fall risks

The summer months have been underscored by a favorable supply and demand backdrop, but that could potentially transition into a defensive posture in the fall should elevated risks arise, according to a new report from BlackRock analysts Peter Hayes, head of the Municipal Bonds Group, James Schwartz, head of municipal credit research and Sean Carney, head of municipal strategy.

Municipals maintained their seasonal trend and posted strong performance throughout the month of July, the analysts noted in Monday’s report.

“The market benefited from a favorable supply-demand backdrop and rallying interest rates due to excess liquidity, short covering, and Delta variant fears,” they wrote. “Tight credit spreads and rich valuations once again acted as a drag, spurring modest underperformance versus comparable Treasury bonds.”

The S&P Municipal Bond Index returned 0.70%, bringing the year-to-date total return to 1.95%, they pointed out. Longer-duration — greater interest-rate sensitivity — and lower-rated bonds outperformed the broader index, they said.

Supply moderated from the robust levels experienced in June and trended more in line with historical expectations, the team explained. Issuance of $35 billion was down by 26% month-over-month, but just 5% above the five-year average — bringing the year-to-date total to $255 billion, according to the report.

Taxable issuance accounted for 27% of supply, the highest level since February, as lower interest rates made advance refunding tax-exempt debt in the taxable municipal market “more economical,” they noted.

As a result, reinvestment income from maturities, calls and coupons “significantly outpaced” tax-exempt issuance and provided a strong technical tailwind, according to Hayes, Schwartz, and Carney.

They said demand remained firm with the asset class garnering continued inflows.

“While fund flows slowed slightly into month end amid lower absolute yields, 2021 remains on pace to eclipse 2019 as the best fund flow year on record,” they said.

Looking ahead, the analysts expect the market will continue to benefit from a near-term supply-demand imbalance. “However, given recent performance strength and current stretched valuations, we anticipate monetizing some of our gains in August, ahead of the less favorable seasonal trends and increased event risks in the fall.”

Secondary bond trading

ICE Data Services reported the following muni trades:

Michigan State Trunk Line Fund Series 2021A 5s of Nov. 15, 2035 [5946952S6] traded in a block of $5 million+ at a price of 135.718, a yield of 1.265%. The Rebuilding Michigan Program 5s were originally priced on Aug. 24 at 136.231, a yield of 1.22%.

The Michigan State Trunk Line Series 2021A 5s of Nov. 15, 2034 [5946952R8] traded in a block of $5 million at a price of 136.346, a yield of 1.210%. The 5s were originally priced on Aug. 24 at 136.461, a yield of 1.20%.

Muni benchmarks

The triple-A benchmark scales were unchanged in light trading on Monday.

According to Refinitiv MMD, short yields were steady at 0.06% and at 0.08% in 2022 and 2023. The yield on the 10-year stayed at 0.88% while the yield on the 30-year sat at 1.50%.

The 10-year muni-to-Treasury ratio was calculated at 70.1% while the 30-year muni-to-Treasury ratio stood at 78.0%, according to MMD.

The ICE municipal yield curve showed bonds steady in 2022 at 0.06% and 0.08% in 2023. The 10-year maturity was at 0.91% and the 30-year yield was at 1.48%.

The 10-year muni-to-Treasury ratio was calculated at 72% while the 30-year muni-to-Treasury ratio stood at 77%, according to ICE.

The IHS Markit municipal analytics curve showed short yields steady at 0.07% and 0.08% in 2022 and 2023, respectively, with the 10-year at 0.90%, and the 30-year yield sat at 1.48%.

In late trading, Treasuries were stronger while equities were mixed.

The 10-year Treasury was yielding 1.26% and the 30-year Treasury was yielding 1.94%. The Dow Jones Industrial Average rose 0.10%, the S&P 500 increased 0.05% while the Nasdaq lost 0.40%.

Primary market

Other larger deals set for pricing this week include:

Miami-Dade County, Fla., which is set to price on Wednesday $202.14 million of Series A-1 (A3//A/), serials 2040-2041, term 2046; $221.330 million of Series A-2 (A3//A/), serial 2046, term 2050; $180.43 million of Series B-1 (Aa3//AA-/), term 2046, 2050; $96.07 million of Series B-2 (Aa3//AA-/), serial 2038-2041, term 2044; $383.23 million of Series A-3 (A3//A/), serial 2023-2036, term 2040; and $159.325 million of Series B-3 (Aa3//AA-/), serial 2025-2038. Wells Fargo Corporate & Investment Banking.

The Kansas Development Finance Authority (Aa3/A+//) is set to price Tuesday $502.655 million of taxable revenue bonds, serials 2022-2036, term 2051. Citigroup.

The City of Houston (Aa3//AA/) is set to price on Tuesday $348.8 million of exempt and taxables consisting of: $179.78 million of public improvement refunding bonds, series 2021A; $166.455 million of taxable public improvement refunding bonds, series 2021B; and $2.565 million of certificates of obligation (Demolition Program), series 2021C. Mesirow Financial.

The Pennsylvania Housing Finance Agency (Aa1/AA+//) is set to price on Wednesday $296.67 million of single-family mortgage revenue social bonds (non-AMT). BofA Securities.

The City of Aurora, Colorado (/AA+/AA+/) through its Utility Enterprise is set to price on Thursday $266.7 million of taxable first-lien water refunding revenue green bonds. Morgan Stanley.

The California Statewide Communities Development Authority (/A-/A/) is set to price $196.285 million of Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The California Statewide Communities Development Authority (/A-/A/) is also set to price $109.61 million of taxable Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The Connecticut Health and Educational Facilities Authority (/BBB+/BBB+/) is set to price on Wednesday $193 million of Stamford Hospital Issue, Series M forward delivery revenue refunding bonds. Goldman Sachs.

The Rhode Island Housing and Mortgage Finance Corp. (Aa1//AA+/) is set to price on Wednesday $172.455 million of exempt and taxable homeownership opportunity social bonds, $144.59 million exempt Series 75-A And $27.865 million of taxable series 75-T. Morgan Stanley.

The CMFA Special Finance Agency VIII is set to price on Tuesday $149.76 million of Essential Housing Revenue Bonds, Series 2021A (Elan Huntington Beach), $99.280 million of 2021A-1 Senior Bonds, term 2056, and $50.48 million of 2021A-2 Junior Bonds, term 2047. Jefferies.

The University of North Dakota (A1///) is set to price on Thursday $144.32 million of certificates of participation: $127,525 million of series A, serial 2024, 2027-2030, terms: 2032,2034,2036,2039,2041,2046,2051,2061 and $16.795 million of refunding series B, 2022-2034. Stifel, Nicolaus & Co.

The Metropolitan District, Hartford County, Connecticut (Aa3/AA//) is set to price on Wednesday $142.445 million of general obligation bonds: $129.53 million of GOs, series 2021A, serials 2022-2041; and $12.914 million of GO refunding forward deliver bonds, Issue of 2021, Series B, serials 2023-2033. Raymond James & Associates.

The Rhode Island Infrastructure Bank (/AAA/AAA/) is set to price $127.965 million of taxable State Revolving Fund Refunding Revenue Bonds, Series 2021A, (Master Trust), serials 2021-2044. Raymond James & Associates.

The Hays Consolidated Independent School District, Texas (Aaa///) (PSF guarantee) is set to price on Tuesday $125 million of unlimited tax school building bonds. FHN Financial Capital Markets.

The City of Carmel, Indiana Local Public Improvement Bond Bank is set to price $122 million of multipurpose bonds, $87.245 million of Series A (/AA//), serials 2024-2041, and $34.8 million of Series B refunding bonds, serials 2022-2041. Stifel, Nicolaus.

The Iowa Finance Authority/Palm Beach County Health Facilities Authority (//BBB/) is set to price on Thursday $120.465 million of Lifespace Communities, Inc. revenue refunding bonds. Ziegler.

The Louisiana Energy and Power Authority (/AA//) is set to price $120.325 million of Power Project Revenue Refunding Bonds (LEPA Unit No. 1) Taxable Series 2021A. Assured Guaranty Municipal Corp. Raymond James.