Municipals faced some pressure and benchmark yield curves were cut by one to two basis points Wednesday. Municipals largely have shrugged off a weaker U.S. Treasury market and outperformed while mutual funds saw another $2 billion-plus week of inflows.

The 10- and 30-year UST have risen nine basis points since Monday, while munis have only inched up one basis point on the 10-year and one to two total on the short end after more than a week of steadiness.

“After months of low yields and credit compression some sellers emerged to take advantage of the low rates well below 1% in the short end and the belly,” said Peter Franks, Refinitiv MMD senior market analyst.

There is still a supply/demand imbalance that will keep munis “in decent, if not guarded shape, and the current ratios are on the higher side of their three-month averages in 10- and 30-years,” Franks noted. Several participants noted investors have come to accept, perhaps begrudgingly, where ratios have settled.

The 10-year muni-to-Treasury ratio was at 66% while the 30-year muni-to-Treasury ratio stood at 77%, according to Refinitiv MMD.

The 10-year muni-to-Treasury ratio was at 69% while the 30-year muni-to-Treasury ratio was at 77%, according to ICE Data Services.

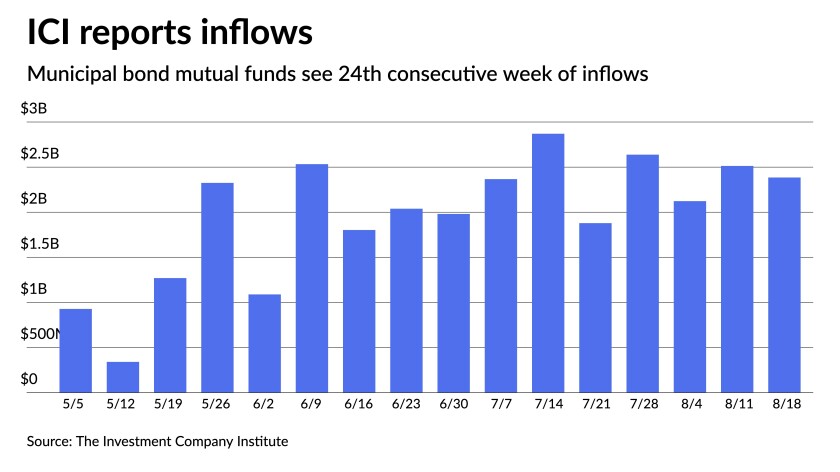

Fund flows continue on a tear, with the Investment Company Institute reporting $2.385 billion of inflows into municipal bond mutual funds for the week ending Aug. 18, down from $2.513 billion the week prior.

It marked the 24th week in a row the funds saw inflows, to reach $67 billion of inflows year-to-date.

Exchange-traded funds saw $513 million of inflows after $210 million the week prior and $105 million the last week of July. A slight drop the prior two weeks had some participants on guard that certain investors, such as insurance companies, were backing out some from the product.

In the primary market, Federal Way SD #210, Washington, (Aaa///) sold $108.95 million of unlimited tax general obligation bonds to Wells Fargo: Bonds in 6/2024 with a 5% coupon yield 0.22%, 5s of 2026 at 0.48%, 4s of 2031 at 1.02%, 2s of 2036 at 1.77% and 2s of 2041 at 2.05%.

In the negotiated market, BofA Securities priced $425.88 million of taxable pension obligation bonds for Santa Ana, California, (/AA//). Bonds in 8/2022 priced at par at 0.247%, at 1.176% in 2026, 2.189% in 2031 and 3.089% in 2044, callable Aug. 1, 2031, subject to make whole call.

BofA Securities priced for North Carolina (A2/AA/A+/) $250.84 million of Series 2021 grant anticipation revenue vehicle bonds: bonds in 3/2022 with a 5% coupon yield 0.05%, 5s of 2026 at 0.43%, 5s of 2031 at 1.10% and 2s of 2036 at 2.10%.

BofA Securities also priced for the South Carolina Public Service Authority (A2/A/A-/) $427 million of tax-exempt revenue obligations, $14.735 million of Series 2021A refunding bonds and $284.555 million of Series 2021B improvement bonds. Bonds in 12/2022 with a 5% coupon yield 0.14%, 5s of 2026 at 0.54%, 5s of 2031 at 1.33%, 4s of 2036 at 1.72%, 5s of 2036 at 1.60%, 4s of 2041 at 1.93%, 4s of 2047 at 2.09%, 5s of 2051 at 2.00% and 4s of 2051 at 2.16%.

Informa: Money market muni funds fall

Tax-exempt municipal money market fund assets fell by $376.9 million, lowering their total to $90.73 billion for the week ending Aug. 24, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds sat at 0.01%, the same as the previous week.

Taxable money-fund assets rose by $983.6 million, bringing total net assets to $4.368 trillion. The average, seven-day simple yield for the 761 taxable reporting funds sat at 0.02%, same as the prior week.

Secondary trading and scales

Secondary trading showed some pressure on bonds inside 15 years. Washington Suburban Sanitation District 5s of 2022 traded at 0.06%. Georgia 5s of 2023 at 0.12%.

Loudoun County, Virginia, 5s of 2027 at 0.60%-0.58%. Maryland 5s of 2028 at 0.65%. Maryland 5s of 2029 at 0.75%-0.73%.

Maryland 5s of 2031 at 0.93% versus 0.91% Monday. New York City TFA 5s of 2032 at 1.18% (at 1.14%-1.13% on Aug. 10). Maryland 5s of 2033 at 1.05% versus 1.04%-1.03% Monday.

Washington 5s of 2034 at 1.20% (1.19%-1.18% on Aug. 10). New York City TFA 5s of 2034 at 1.27% versus 1.22% original.

Washington 5s of 2042 at 1.51%-1.43%. California 5s of 2043 at 1.43%. Dallas water 3s of 2046 at 2.01% versus 1.91% original.

New York City 5s of 2047 at 1.89% versus 1.90% original. Los Angeles Department of Water and Power 5s of 2049 at 1.53%. Georgia road and tollway 3s of 2050 traded at 2.01%.

Short yields were cut a basis point to 0.07% in 2022 and one basis point to 0.10% in 2023 on Refinitiv MMD’s scale. The yield on the 10-year rose one to 0.89% while the yield on the 30-year sat at 1.50%.

The ICE municipal yield curve showed bonds up one basis point in 2022 at 0.07% and to 0.10% in 2023. The 10-year maturity rose one basis point to 0.92% and the 30-year yield was at 1.50%.

The IHS Markit municipal analytics curve showed short yields up one basis point to 0.07% and 0.09% in 2022 and 2023, respectively. The 10-year yield rose one to 0.91% and the 30-year yield one to 1.50%.

The Bloomberg BVAL curve showed short yields rise one to 0.07% and 0.07% in 2022 and 2023. The 10-year yield rose two to 0.91% and the 30-year yield at 1.49%.

In late trading, Treasuries were softer as equities again traded higher.

The 10-year Treasury was yielding 1.347% and the 30-year Treasury was yielding 1.952%. The Dow Jones Industrial Average gained 39 points or 0.11%, the S&P 500 increased 0.22% while the Nasdaq gained 0.15%.

Don’t expect much from Jackson Hole

While last year’s Jackson Hole symposium provided news about the Federal Reserve’s switch to an inflation average monetary policy, don’t expect “any breaking insights into the Fed’s outlook for the economy, inflation, or the Fed’s conduct of monetary policy,” said Berenberg chief economist for the U.S., Americas and Asia Mickey Levy, a member of the Shadow Open Market Committee.

“Under current circumstances of a solid recovery in labor markets and inflation far above the Fed’s 2% longer-run target, we think it would be appropriate and timely for [Federal Reserve Board Chair Jerome] Powell to provide detail on how and when the Fed will begin to unwind its emergency monetary policies, including tapering its asset purchases and also provide guidelines on the Fed’s plans to normalize interest rates under different scenarios,” he said. “However, it is most likely that Powell’s speech will stick to the Fed’s recent script of tip-toeing toward tapering and disassociating the unwinding of its asset purchases from the eventual liftoff of rates.”

While Powell will likely have an “upbeat” economic outlook, it will be tempered by concern about the Delta variant of COVID-19, which could “temporarily dampen near-term activity,” Levy said.

Powell could acknowledge the improvement in the labor markets and may say that the substantial further progress term was met with the July employment numbers, he added, and an announcement on tapering could be forthcoming “if everything goes well,” but won’t offer a timeline.

“Powell is also likely to repeat recent guidance that the timing of the tapering will not imply anything about when the Fed will begin raising the Fed funds rate, which has been anchored to zero since March 2020,” Levy said.

A taper announcement is expected by Levy at the September or November Federal Open Market Committee meeting, with tapering beginning by year end. “The Fed may delay this unwinding if the Delta variant transmission continues to spike and rise and dampen economic growth more than expected,” he said.

Craig Erlam, senior market analyst, UK & EMEA, at OANDA, agreed. “Frankly, I wouldn’t be surprised if this turns out to be one big anticlimax, with Powell saying very little of note and instead insisting that the data will dictate any decisions in the upcoming meetings.”

And others also see the taper announcement coming after Jackson Hole. “The September FOMC meeting might be a good time to announce a taper starting in November, unless the August employment report is a dud,” said Joe Kalish, chief global macro strategist at Ned Davis Research (NDR).

Hear more of Joe’s thoughts on this Bond Buyer podcast.

NDR expects the Fed to cut its Treasury purchases by $10 billion each month and mortgage-backeds by $5 billion, meaning tapering would be done in eight months, but could be adjusted if either the labor or inflation picture changes.

“Powell will need to emphasize that the bar for raising rates is higher than it is for tapering,” Kalish said, “and that rate hikes do not automatically follow the completion of tapering.”

By discussing tapering, the Fed averted a possible taper tantrum, said John Vail, chief global strategist at Nikko Asset Management. “No one is expecting much new information during the conference.”

With vaccines available, shutdowns become less likely, he said. “Already, many zero-tolerance countries are realizing such cannot continue and more are adapting to a ‘living with COVID’ theme, (much as what Japan has been doing) concentrating on preventing the most risky aspects,” he said.

Wilmington Trust says the November meeting “seems more plausible” for a taper announcement, says CIO Tony Roth, “as it would provide more time for the Fed to assess progress on the labor market and the impact of the Delta variant (both of which still have potential to change the timing of the Fed’s taper timing.”

Indeed, Federal Reserve Bank of Dallas President Robert Kaplan, an early proponent of the need to taper, last week said if the Delta variant continues to slow the economy he could change his mind about a September announcement, Roth said.

The lone indicator released Wednesday, durable goods orders slipped 0.1% in July after a revised 0.8% gain in June, first reported as a 0.9% increase.

Economists polled by IFR Markets expected a 0.2% decline.

Excluding transportation, orders rose 0.7% after a 0.6% gain, first reported as a 0.5% rise. Economists expected a 0.5% increase.

“This is only the second time since the initial reopening of the economy in May of last year that durable goods orders posted a decline,” noted Wells Fargo Securities Senior Economist Tim Quinlan and Economist Shannon Seery. “The scant 0.1% dip in orders for durable goods is remarkable after accounting for the fact that civilian aircraft orders fell by about half during the month.”

Core capital goods orders were unchanged in the month, “but the run-up in goods consumption during the pandemic has resulted in a speedy rebound in orders to date.”

Grant Thornton Chief Economist Diane Swonk agreed. “Durable goods orders and shipments suggest that manufacturers are beginning the long, arduous process of replenishing empty shelves,” she said. “How long that takes and what it means for inflation has been complicated by the Delta variant. Higher prices and an end to stimulus checks are also taking a toll on demand.”

Primary to come:

The Utah Military Installation Development Authority is set to price $260 million of tax allocation and hotel tax revenue Series 2021A-1 and tax allocation revenue bonds Series 2021A-2. Piper Sandler

Love Field Airport Modernization Corp. is set to price $246.72 million of Series 2021 AMT general airport revenue refunding bonds (/A-/). BofA Securities.

New York City Housing Development Corp. is set to price $200 million of Series 2021 Series G multifamily housing revenue bonds (Aa2///). Ramirez & Co.

The North Carolina Housing Finance Agency (Aa1/AA+//) is set to price $150 million of home ownership revenue bonds, series 47 (non-AMT) (1998 Trust Agreement), serials 2022-2033, terms 2036, 2041, 2044, 2051. Wells Fargo Corporate & Investment Banking.

Denton, Texas, (/A+/A+/) is set to price $141 million of utility system revenue refunding bonds, taxable series 2021. Citigroup Global Markets Inc.