Municipals were little changed in light trading on the last Friday of August as U.S. Treasuries made gains as did equities following Federal reserve Board Chair Jerome Powell’s Jackson Hole speech.

The total potential volume for next week is estimated at $4.938 billion, an expected drop as the unofficial final week of summer comes ahead of Labor Day weekend.

It’s led by $1.2 billion of exempt and taxable New York City Transitional Finance future tax-secured bonds. The TFA also brings the largest competitive loan of the week with its $250 million of taxables.

There are $3.826 billion of negotiated deals scheduled and $1.111 billion of competitive loans.

A few notable deals include a $400 million-plus nonrated senior living from the New Hope Cultural Education Facilities Finance Corp. in Texas and newly upgraded Wisconsin with a $327.4 million of taxable general obligation refunding on Tuesday.

While 30-day visible supply sits at a meager $7 billion, the supply/demand gap should ease some going into September, according to BofA Securities in a weekly municipal report.

New issuance is expected to be $41 billion, BofA says, but principal redemptions are expected to be only about $20 billion and coupon payments about $8 billion, significantly lower than any of the previous three months (August alone was north of $60 billion of cash).

Even with fewer redemptions and more supply, however, “this is unlikely to affect pricing much due to continued strong mutual fund flows and high cash levels in institutional and retail portfolios,” strategists Yingchen Li and Ian Rogow said in the report.

In the next few weeks, BofA expects muni/Treasury ratios to move lower and credit spreads to go tighter “as volatilities should decline and a risk-on atmosphere returns to the macro landscape.”

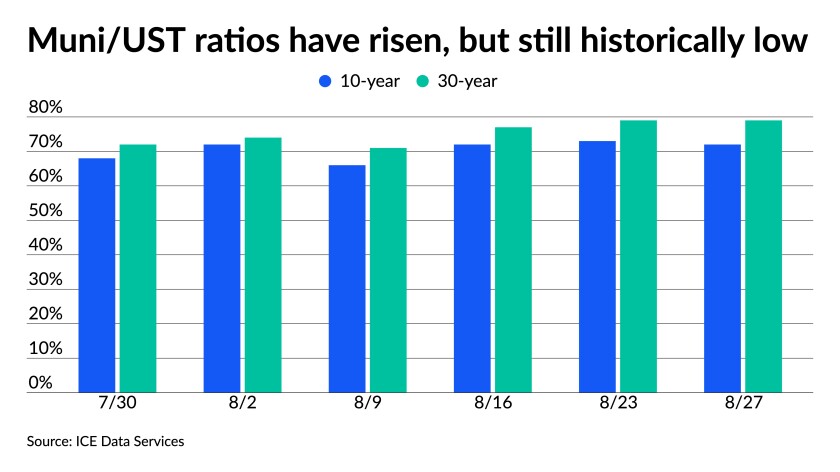

Ratios were little changed Friday with the 10-year muni-to-Treasury ratio at 69% and the 30-year at 79%, according to Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 72% while the 30-year was at 79%, according to ICE Data Services.

Although munis have remained quite rich for the past few months, they are still more attractive than Treasuries or corporates, BofA said.

Secondary trading and scales

Sparse trading showed levels little changed. Fairfax County, Virginia, 5s of 2022 traded at 0.08%. District of Columbia 5s of 2026 at 0.42%. Washington 5s of 2026 at 0.49%-0.46%.

New York City TFA 5s of 2032 at 1.22%-1.21%. California 5s of 2041 at 1.43%-1.44%. Frisco, Texas, ISD 2s of 2043 at 2.16%.

New York City 5s of 2047 at 1.90%-1.80% versus 1.90% original.

Dallas waterworks 3s of 2050 at 2.01% versus 2.03%-2.02% Thursday.

Short yields were steady at 0.07% in 2022 and 0.10% in 2023 on Refinitiv MMD’s scale. The yield on the 10-year stayed at 0.91% while the yield on the 30-year sat at 1.52%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.08% and 0.11% in 2023. The 10-year maturity sat at 0.92% and the 30-year yield was at 1.50%.

The IHS Markit municipal analytics curve showed short yields steady at 0.07% and 0.09% in 2022 and 2023. The 10-year yield steady at 0.92% and the 30-year yield steady at 1.51%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield rose stayed at 0.92% and the 30-year yield at 1.51%.

In late trading, Treasuries were better as equities gained.

The 10-year Treasury was yielding 1.308% and the 30-year Treasury was yielding 1.914%. The Dow Jones Industrial Average gained 249 points or 0.71%, the S&P 500 rose 0.91% while the Nasdaq gained 1.30%.

The main event

Everyone agrees Federal Reserve Board Chair Jerome Powell said the Fed could start tapering this year and that it would have no implications for liftoff, but not everyone was satisfied with what they heard.

“The speech supported the Fed’s assertion that the sharply higher inflation is temporary, and that inflationary expectations remained well anchored to the Fed’s longer-run objective,” noted Berenberg chief economist for the U.S., Americas and Asia Mickey Levy, a member of the Shadow Open Market Committee. “In this regard, parts of the speech seem strained and display an asymmetric assessment of the risks.”

“Markets of course were looking for signals of when the Fed would begin tapering,” he added. “Powell did not provide any indication.”

Powell “gave the general impression that though the Fed has been on the verge of announcing the start of tapering, it won’t take that step until it’s evident that the current COVID outbreak won’t cause a further economic dip,” said Cato Senior Fellow and Director of the Center for Monetary and Financial Alternatives George Selgin. “A rate liftoff remains a still more distant prospect.”

Should consumer prices continue rising “relatively rapidly,” he said. “It may even be compelled to alter some of its policy rate settings, if only by means of ‘technical adjustments’ that leave its official target range unchanged.”

And while other Fed officials, mostly non-voters, were on television professing their desire to cut back on asset purchases, while Powell “may be joining the consensus,” said Interactive Brokers’ Chief Strategist Steve Sosnick, “he sounded less aggressive than his FOMC peers. Most importantly, he does not see the conditions that are necessary for interest rate hikes anytime soon.”

“In what would have been a perfect opportunity for the Fed to provide greater clarity on changes to their asset purchase program, Powell erred on the side of caution,” said Dustin Qualley, senior portfolio manager at Build Asset Management, which focuses on fixed-income and options strategies.

“I would have liked to hear more about how the Fed sees their policies evolving to address the structural changes in the economy where many Americans are still faced with joblessness,” he said.

The Jackson Hole address accelerates the move toward tapering, said Sebastien Galy, senior macro strategist at Nordea Asset Management, “putting the September meeting well in play.”

However, he had an issue with the continuing expectation inflation will be transitory. “They cannot take the spike in inflation to be temporary as granted.”

But Lee Ferridge, head of Macro Strategy for North America at State Street Global Markets, said Powell “nailed it.”

“He managed to bring forward (albeit by only a month or two) market expectations for the taper timing but, markets still rallied,” Ferridge said. “That, I suspect, would have been his objective ahead of the speech: increase taper expectations (it has been a slow drip process since June) but not cause a taper tantrum. He succeeded on both fronts.”

The key, he said, was stressing taper would have no impact on liftoff and “by talking down inflation risks at the same time that he is arguing for a taper. He laid out the case for current inflation pressures being transitory and also argued that there was little sign of wages gains that were necessary to fuel ongoing inflation. So, he managed to announce a (slightly) more hawkish policy shift, while at the same time laying out why he is likely to remain a medium/long-term dove. A job well done.”

In the speech, Powell said, “Long-term unemployment remains elevated, and the recovery in labor force participation has lagged well behind the rest of the labor market, as it has in past recoveries.” But, the factors keeping people from looking for a “are likely fading,” although “the Delta variant presents a near-term risk, the prospects are good for continued progress toward maximum employment.”

The inflationary pressures seen by businesses and consumers, he said, is “a cause for concern,” but the high levels should “prove temporary” and his “baseline outlook is for continued progress toward maximum employment, with inflation returning to levels consistent with our goal of inflation averaging 2% over time.”

Data should support his belief “some of the supply-demand imbalances are improving, and [offer] more evidence of a continued moderation in inflation, particularly in goods and services prices that have been most affected by the pandemic.”

Policy, he said, “is well positioned,” although the Fed is prepared if adjustments are needed.

Powell said inflation has met the “substantial further progress” level, and while “clear progress” was made in employment “we have much ground to cover to reach maximum employment.”

At the July FOMC meeting, he said, most of the officials, including him, thought “if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.” Since then, there’s been “more progress in the form of a strong employment report for July, but also the further spread of the Delta variant.”

The taper “will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test,” Powell said. “We have said that we will continue to hold the target range for the federal funds rate at its current level until the economy reaches conditions consistent with maximum employment, and inflation has reached 2% and is on track to moderately exceed 2% for some time. We have much ground to cover to reach maximum employment, and time will tell whether we have reached 2% inflation on a sustainable basis.”

In data released Friday, personal income gained 1.1% in July after a 0.2% rise in June, while spending rose 0.3% in the month after a 1.1% jump in June.

The PCE price index rose 0.4% in the month after a 0.5% gain in June, while the core PCE climbed 0.3% after a 0.5% increase, while for the year PCE rose 4.2% and core gained 3.6% In June the annual PCE was up 4.0% and core rose 3.6%.

Economists polled by IFR Markets expected income up 0.2% and spending 0.3% higher, the core PCE price index to be up 0.3% for the month and 3.6% for the year.

The report “provides a clear signal that real (inflation adjusted) consumption has flattened, while inflation continues to rise,” said Berenberg’s Levy. “Although strong job gains and rising wages are boosting gains in personal income, real spending has slowed, presumably reflecting supply constraints and higher product prices, and inflation shows no signs of decelerating.”

PCE numbers he said have been “dramatically higher than earlier forecasts” and with low numbers posted in the last five months of 2020, expect more increases in the months ahead, he said.

While spending rose in the month, “inflation grew even faster,” said Wells Fargo Securities Senior Economist Tim Quinlan and Economist Shannon Seery. “The good news is that with income up 1.1% on the month, consumers could bankroll more spending; the bad news is that they are disinclined to do so.”

Whether or not inflation proves to be transitory, they said, “if inflation continues to outpace spending growth, it will become increasingly difficult for the Fed to favor its employment mandate if it means the consumer’s purchasing power is being eaten away by higher prices.”

Also released Friday, the University of Michigan consumer sentiment index closed August at 70.3, up a tick from the mid-month read, but down from July’s 81.2.

Economists expected a 70.9 read.

The current conditions grew to 78.5 from a 77.9 mid-month read, but was down from July’s final read of 84.5, while the expectations index decreased to 65.1 from 65.2 mid-month and 79.0 in July.

Primary market to come

The New York City Transitional Finance Authority (Aa1/AAA/AAA/) is set to price on Wednesday $950 million of future tax-secured subordinate bonds, serials 2023-2027, 2034-2042, terms 2045, 2048. Retail on Monday and Tuesday. RBC Capital Markets.

The TFA is also set to sell $250 million of taxable future tax-secured bonds at 10:45 a.m. Eastern on Wednesday.

The New Hope Cultural Education Facilities Finance Corp., Texas, (nonrated) is set to price $483.535 million of Sanctuary LTC project senior living revenue bonds on Wednesday, consisting of: $413.515 million of Series S21A1, serials 2025-2057; $16.95 million Series S21A2, serials 2022-2025; and $53 million of Series S21B, serials 2022-2057. HilltopSecurities.

Wisconsin (Aa1/AA+//AAA) is set to price $327.4 million of taxable general obligation refunding bonds on Tuesday, serials 2023, 2027-2036. Stifel, Nicolaus & Company, Inc.

The New Jersey Healthcare Facilities Authority (/AA-/AA-/) is set to price on Tuesday $200.46 million of Atlanticare Health System Obligated Group revenue bonds. BofA Securities.

The California Community Housing Agency is set to price $143.92 million of essential housing revenue bonds (Summit at Sausalito Apartments), $85.4 million of Series 2021A-1 senior bonds, term 2057 and $58.52 million of Series 2021A-2 junior bonds, term 2050. Jefferies LLC.

American Municipal Power, Inc., Ohio, (/A//) is set to price on Tuesday $141.55 million of Prairie State Energy Campus project revenue refunding bonds. BofA Securities.

Santa Cruz County, California, (/AAA//) is set to price $124.19 million of taxable pension obligation bonds on Thursday. Serials 2022-2036, terms 2041, 2047. Stifel, Nicolaus & Company, Inc.

New Orleans (A2/A+/A/) is set to price on Wednesday $120.9 million of taxable limited tax refunding bonds, serials 2022-2030. Loop Capital Markets

Akron, Ohio, (/AA-//) is set to price $113.265 million of community learning center income tax revenue refunding forward delivery bonds, serials 2022-2033. Stifel, Nicolaus & Company, Inc.

In the competitive market Tuesday, Miami-Dade County, Florida, (/AA/) is set to sell $113.73 million of Public Health Trust general obligation bonds at 10:30 a.m. Eastern.

Cary, North Carolina, (Aaa/AAA/AAA/) is set to sell $125 million of general obligation bonds at 11 a.m.

Harrisonburg, Virginia, (Aa2/AA+//) is set to sell $153.945 million of general obligation bonds at 10:45 a.m.

The South Carolina Association of Governments is set to sell $147.202 million of certificates of participation (MIG-1) at 11 a.m.

On Thursday, Fremont Unified School District, California, is set to sell $116 million of taxable refunding bonds at 12:30 p.m.