Municipals were little changed on light trading in the secondary again Wednesday as Illinois and Texas priced bonds in the primary and the Investment Company Institute reported another round of billion-dollar-plus inflows.

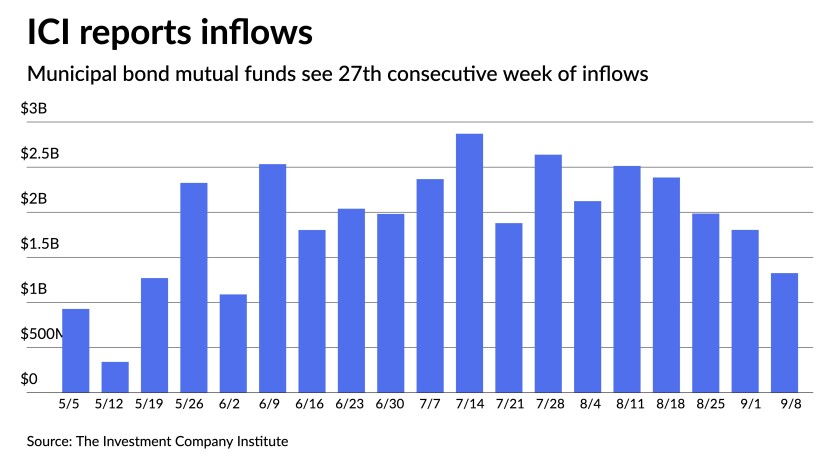

The Investment Company Institute reported $1.325 billion of inflows for the week ending Sept. 8, following $1.804 billion of inflows the prior week, bringing the total to $72 billion year-to-date.

Exchange-traded funds saw $250 million of inflows after $251 million a week prior.

While falling to the lowest total since June 2, the total for the year is still on pace to near or break the record, $93.2 billion, hit in 2019.

With an up-and-down U.S. Treasury market, municipals have yet to move hard in either direction. Triple-A benchmarks were little changed on the day once again. Ratios hovered at recent levels with the 10-year at 71% and the 30-year at 82%, according to Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 76% while the 30-year was at 81%, according to ICE Data Services.

Over the last 30 days and counting, the 10- and 30-year AAA spots have traded in a narrow four to five basis point range, creating less momentum in either direction, said Kim Olsan, senior vice president at FHN Financial.

“Looking ahead to the end of the quarter, volatility remains a key component,” Olsan said. “A stagnant curve for several months running will likely find a catalyst in Q4 — whether it be driven by stepped up issuance or waning fund flows drawing demand away.”

That has yet to happen, but BlackRock also added to a more cautious tone for the municipal market heading into the final stretch of 2021.

“We maintain a defensive posture over the near term amid rich valuations, tight credit spreads, and less historically favorable supply/demand and interest rate dynamics in the fall,” wrote Peter Hayes, James Schwarz and Sean Carney. “We acknowledge the potential for increased volatility stemming from elevated political, fiscal and monetary policy, and COVID-19-related uncertainties. However, we maintain a favorable view of the asset class over the medium term amid improved credit fundamentals and continued strong demand for tax shelter.”

The firm said it has shifted to a “slightly short-of-neutral stance on duration” within a barbell yield curve strategy.

“We continue to hold a preference for lower-rated credits and sectors that have been more impacted by the pandemic, such as transportation, education, travel-related (hotel tax, airport, etc.) and health care,” they said.

In the primary Wednesday, Illinois and Texas, issuers on the polar opposite ends of the ratings spectrum, priced $143 million and $216 million of general obligation bonds, respectively, in a market that has rewarded both high-grades and high-yield. Illinois saw its 10-year maturing in June price plus-45 to triple-A benchmarks while Texas came with its 5s of 2031 maturing in August at 1.10%, or plus 17 basis points.

The shorter end of the curve, the tighter the spreads with Texas coming with a 5% coupon five-year maturing at 0.51% versus Illinois’ five year, same coupon, at 0.67%.

Raymond James & Associates, Inc. priced for Texas (Aaa/AAA/AAA/) $216.083 million of general obligation bonds, consisting of $31.315 million of water financial assistance bonds, Series 2021A: 4s of 8/2022 yield 0.12%, 5s of 2026 at 0.51%, 5s of 2031 at 1.10%, 3s of 2036 at 1.65%, 3s of 2041 at 1.83%, 2.375s of 2046 at 2.38%, callable in 8/1/2031.

The second, $168.953 million of water financial assistance refunding bonds, Series 2021B, saw 4s of 2/2022 at 0.11%, 4s of 2026 at 0.48%, 4s of 2031 at 0.75%, 2s of 2036 at 2.05%, 2.125s of 2038 at 2.12%, callable in 8/1/2025.

The last, $15.815 million of water financial assistance refunding bonds (Economically Distressed Areas Program), Series 2021, saw 4s of 8/2022 at 0.12%, 5s of 2026 at 0.51% and 2s of 2029 at 0.91%, noncall.

Ramirez & Co., Inc. priced for Illinois (/BBB+/BBB+/AA+) $143.045 million of Build Illinois Bonds sales tax revenue bonds, junior obligation: Bonds in 6/2022 with a 5% coupon yield 0.15%, 5s of 2026 at 0.67%, 5s of 2031 at 1.38% and 4s of 2033 at 1.65%.

U.S. Bancorp Investments Inc. priced for the City of Farmington, New Mexico (Baa2/BBB//) $140 million of pollution control revenue refunding bonds (Public Service Company of New Mexico San Juan and Four Corners Projects). Bonds in 4/2033 priced at 2.15% par, callable 10/1/2031.

Informa: Money market muni funds fall

Tax-exempt municipal money market fund assets fell by $894.8 million, lowering their total to $89.8 billion for the week ending Sept. 14, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds sat at 0.01%, the same as the previous week.

Taxable money-fund assets rose by $572.6 million, bringing total net assets to $4.361 trillion. The average, seven-day simple yield for the 760 taxable reporting funds sat at 0.02%, same as the prior week.

Secondary trading and scales

California 4s of 2022 traded at 0.06%. Minnesota 5s of 2024 at 0.18%.

Washington 5s of 2027 at 0.55%. Minnesota 5s of 2028 at 0.69%. Columbus Ohio 5s of 2028 at 0.66%. Washington Suburban Sanitation District 5s of 2028 at 0.67%. Wisconsin green bond 5s of 2029 at 0.75% (last traded in blocks on 8/24 at the same level.)

Minnesota 5s of 2031 at 0.97%.

Seattle 4s of 2034 at 1.25% (1.24% on 8/25.) New York City 5s of 2034 at 1.43%.

Michigan trunk line 5s of 2035 at 1.28%.

California 5s of 2043 at 1.44%. New York City TFA 4s of 2048 at 2.01% versus 2.00%-1.99% Tuesday.

Triborough Bridge and Tunnel 5s of 2051 at 1.82%.

Refinitiv MMD’s scale showed short yields steady at 0.08% in 2022 and 0.11% in 2023. The yield on the 10-year fell sat at 0.93% while the yield on the 30-year stayed at 1.53%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.09% and at 0.12% in 2023. The 10-year maturity sat at 0.95% and the 30-year yield was at 1.52%.

The IHS Markit municipal analytics curve showed short yields steady at 0.09% and 0.11% in 2022 and 2023. The 10-year yield at 0.93% and the 30-year at 1.52%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield sat at 0.93% and the 30-year yield stayed at 1.52%.

The 10-year Treasury was yielding 1.303% and the 30-year Treasury was yielding 1.869% in late trading. The Dow Jones Industrial Average gained 266 points or 0.77%, the S&P 500 rose 0.92% while the Nasdaq gained 0.88%.

Economic indicators

Business activity and employment in New York increased in September as signs the state’s economy was beginning to recover were evident in data released on Wednesday.

The Federal Reserve Bank of New York’s Empire State Manufacturing Survey’s labor market indicators showed strong growth in employment and the average workweek this month.

The index for the number of employees rose eight points to 20.5 while the average workweek index jumped 15 points to 24.3.

Overall business activity surged too, with the general business conditions index up 16 points to 34.3 last month from 18.3 in August. Economists surveyed by IFR Markets had forecast a reading of 18.0.

The prices paid index held steady at 75.7 while the prices received index increased two points to 47.8, its third straight record high.

Looking ahead, the index for future business conditions was little changed at 48.4, pointing to ongoing optimism about the six-month outlook. The capital expenditures index rose 11 points to a multi-year high of 33.9 while the technology spending index rose 18 points to a record high of 33.0.

Also Wednesday, the Federal Reserve reported that industrial production increased 0.4% in August after rising 0.8% in July.

Economists polled by IFR Markets has expected a gain of 0.4% last month.

“Late-month shutdowns related to Hurricane Ida held down the gain in industrial production by an estimated 0.3 percentage point,” the Fed said. “Although the hurricane forced plant closures for petrochemicals, plastic resins, and petroleum refining, overall manufacturing output rose 0.2%. Mining production fell 0.6%, reflecting hurricane-induced disruptions to oil and gas extraction in the Gulf of Mexico. The output of utilities increased 3.3%, as unseasonably warm temperatures boosted demand for air conditioning.”

Additionally on Wednesday, the Labor Department said import prices fell 0.3% in August after a rise of 0.4% in July.

Lower fuel prices led the decline last month.

Import fuel prices dropped 2.3% in August after a 3.0% rise in July. The August drop was the first monthly decrease since October 2020.

The August downturn was mostly driven by lower petroleum prices. Prices for import petroleum declined 2.4% in August, after advancing 2.3% in July.

The price index for natural gas also fell, dropping 0.8% after a 16.6% surge in July.

Over the past year, prices for import fuel have risen 56.5%. Petroleum prices have increased 55.9% and prices for natural gas are up 93.2% from August 2020.

Meanwhile, prices for U.S. exports increased 0.4% in August, after rising 1.1% in July. Economists polled by IFR Markets has expected a gain of 0.3% in import prices and a gain of 0.5% in export prices.