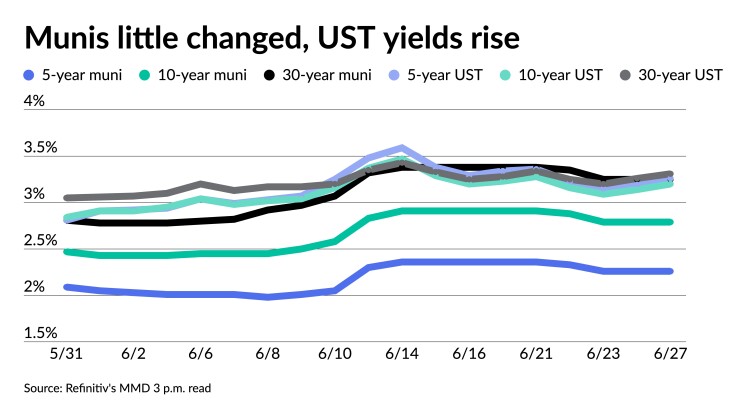

Municipals were lightly traded and little changed steady Monday, while U.S. Treasury yields rose and equities ended in the red.

With the muni triple-A yield curve unchanged out long, and UST seeing small losses, ratios dipped below 100% on the 30-year. Muni-UST ratios were at 69% in five years, 87% in 10 years and 98% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 70%, the 10 at 87% and the 30 at 98% at a 4 p.m. read.

“Although we had a small rally, we should still should understand the fact that we are still not at the bottom, but we are almost there,” said Jason Wong, vice president of Municipals at AmeriVet Securities. “With mounting concerns of a recession and the rally in Treasuries in the last two weeks, we could see munis follow suit as investors are starting to see buying opportunities.”

Average daily Municipal Securities Rulemaking Board trade volume rose 8% last week from the week prior and was 44% higher than the one-year average. Average daily fixed-rate bond trading was up 10% from the week ended June 17, said Pat Luby, a senior municipal strategist at CreditSights.

He notedthat the pace of institutional bid wanteds slowed down last week, with the average daily total par amount down 26% from the prior week. They were still 45% higher than the one-year daily average, per Bloomberg data, he noted.

“The outperformance of munis undermined the relative value of tax-exempts versus corporates,” said Luby.

“Based on the BVAL benchmark yield curves, for investors subject to the 21% federal corporate income tax, tax-exempt munis are still offering a modest advantage at the long end of the double- and single-A yield curves,” he noted.

“If this week’s higher-quality new issues are priced at a concession to the benchmark curves,” he said, “yields could be competitive with comparably rated corporates, which should attract incremental demand from credit investors seeking to add muni risk to their portfolios.”

The calendar is larger to end the quarter at about $8 billion while 30-day visible supply sits at $13.47 billion.

Yield levels on the front end of the curve now hover near 13-year highs, noted Morgan Stanley investment strategists Matthew Gastall and Daryl Helsing in a report. The higher yields are offering investors much higher taxable equivalent yields.

“Some callable, five-year moral obligations of states currently trade with highest-bracket taxable equivalent yields of nearly 6%,” while “certain high-quality dedicated tax structures are presently offering 10-year yield ‘kicks’ that touch TEYs of almost 9% for the high-tax residents of their respective sovereigns,” they said.

Yield levels, they noted, may keep rising while volatility persists, but they think it “continues to be an advantageous period for buy-and-hold investors of individual municipal bonds to gradually, but selectively, add exposure to our market.”

“Maintaining such a long-term perspective may prove itself to be beneficial now that recession risks loom, municipal supply may soon decline, and after the Fed recently stressed that it is ‘strongly committed to fighting inflation,” Gastall and Helsing wrote. “Rather than succumbing to tunnel vision, we feel it’s important to consider the entire investment equation and maintain a long-term focus.”

Iindividual investors “currently enjoy the ‘right of way’ to add some exposure before the summer due to “municipal relative-value ratios to USTs, bearish spring seasonals, healthy public finance credit conditions and higher nominal interest rates,” they said.

Munis outperformed this month’s early UST weakness, but “healthy supply and laggard fund outflows recently helped the asset class to underperform interest-rate movements yet again,” they said.

Ten-year triple-A-rated munis, they said, “are currently offering nearly 90% of the yield of 10-year USTs,” in spite of offering the federal tax exemption. The long-term average for this relationship is a lower 84%, they noted.

“Investor interest and primary market activity often accelerate in the spring, which frequently converges with lower reinvestment demand due to the absence of mid-year/year-end coupon and maturity payments,” they said.

A bearish investment setting and elevated ratios often represent a “buy signal, particularly when strong revenue collections and the passage of healthy stimulus packages have helped to bolster many municipal credit profiles throughout the last two years,” according to Gastall and Helsing.

Short-end muni yields are now near their highest levels since 2008. “Not only are nominal rates of return higher, but price volatility may be relatively limited for bonds whose maturities are set to be redeemed in the near future,” they said.

Moving forward, they noted that “municipal prices may exhibit resiliency if economic recession risks increase, new-issue supply declines this summer, and if the Fed continues to aggressively combat inflation.”

Secondary trading

Georgia 5s of 2023 at 1.67%-1.63% versus 1.63% Friday. Utah 5s of 2024 at 1.96%-1.94%. Fairfax County, Virginia, waters 5s of 2025 at 2.17%.

Prince George’s County, Maryland, 5s of 2027 at 2.25% versus 2.31% Thursday. Georgia 5s of 2031 at 2.77% versus 2.75%-2.74% Friday and 2.83% original.

Los Angeles Department of Water and Power 5s of 2040 at 3.52%. Washington 5s of 2042 at 3.54%-3.51%.

LA DWP 5s of 2047 at 3.75%. Charleston, S.C., waters 5s of 2052 at 3.56% versus 3.58%-3.53% Friday and 3.75% original.

AAA scales

Refinitiv MMD’s scale was little changed at the 3 p.m. read: the one-year at 1.62% (-1) and 1.97% (unch) in two years. The five-year at 2.26% (unch), the 10-year at 2.79% (unch) and the 30-year at 3.25% (unch).

The ICE municipal yield curve was little changed: 1.65% (unch) in 2023 and 1.97% (unch) in 2024. The five-year at 2.31% (unch), the 10-year was at 2.76% (+1) and the 30-year yield was at 3.25% (unch) at a 4 p.m. read.

The IHS Markit municipal curve was unchanged: 1.63% in 2023 and 1.97% in 2024. The five-year at 2.24%, the 10-year was at 2.80% and the 30-year yield was at 3.26% at 4 p.m.

Bloomberg BVAL was also unchanged: 1.65% in 2023 and 1.95% in 2024. The five-year at 2.28%, the 10-year at 2.79% and the 30-year at 3.25% at a 4 p.m. read.

Treasuries were slightly weaker.

The two-year UST was yielding 3.120% (+6), the three-year was at 3.210% (+7), the five-year at 3.254% (+7), the seven-year 3.265% (+6), the 10-year yielding 3.195 (+6), the 20-year at 3.566% (+5) and the 30-year Treasury was yielding 3.309% (+5) at 4 p.m.

Primary to come:

The New York City Transitional Finance Authority (Aa1/AAA/AAA/) is set to price Wednesday $950 million of future tax-secured tax-exempt subordinate bonds, Fiscal 2023 Series A, Subseries A-1, serials 2024-2028. Siebert Williams Shank & Co.

The Alabama Corrections Institution is set to price Tuesday $725 million of Finance Authority revenue bonds, Series 2022A, serials 2022-2023 and 2026-2052. Stephens.

The Municipal Electric Authority of Georgia (A2/A/BBB+/) is set to price Tuesday $369.005 million of Plant Vogtle Units 3 & 4 bonds, consisting of Project M bonds, Project J bonds, Project P bonds and taxable Project P bonds. Goldman Sachs.

The Beaverton School District No. 48J, Oregon, (Aa1/AA+//) is set to price Tuesday $318.172 million of general obligation bonds, consisting of $139.147 million of deferred interest bonds, Series 2022A and $179.025 million of current interest bonds, Series 2022B, insured by Oregon Bond Guaranty Act. Piper Sandler & Co.

The Alameda Corridor Transportation Authority, California, is set to price Thursday $273.500 million of lien revenue refunding bonds, consisting of tax-exempt senior capital appreciation bonds, Series 2022A (A3/A-/A/); taxable senior current interest bonds, Series 2022B (A3/A-/A/); and tax-exempt second convertible capital appreciation bonds, Series 2022C (Baa2/BBB+/BBB/). J.P. Morgan Securities.

The Sumter County Industrial Development Authority, Florida, (B1/B+/BB-/) is set to price Thursday $250 million of green exempt Enviva Inc. Project facilities revenue bonds, Series 2022, serial 2052. Citigroup Global Markets.

Texas (Aaa///) is set to price Tuesday $250 million of Texas Veterans Land Board veterans bonds, Series 2022, Weekly VRDB, term 2053. Jefferies.

The San Diego Unified School District, California, is set to price Thursday $235 million of 2022-2023 tax and revenue anticipation notes, Series A, serial 2023. Citigroup Global Markets.

The New Hope Cultural Education Facilities Finance Corp., Texas, is set to price Wednesday $197.915 million of Outlook at Windhaven Project retirement facility revenue bonds, Series 2022, consisting of $109.715 million of Series 2022A, $19.755 million of Series 2022B-1, $25.640 million of Series 2022B-2, $41.465 million of Series 2022B-3 bonds and $1.340 million of Series 2022C. Ziegler.

The Dormitory of the State of New York (/BBB-//) is set to price Wednesday $148.815 million of Yeshiva University revenue bonds, Series 2022A. Goldman Sachs & Co.

The Merrillville Multi-School Building Corp., Indiana, (/AA+//) is set to price Tuesday $145.495 million of ad valorem property tax first mortgage bonds, Series 2022, serials 2028-2042, insured by Indiana State Aid Intercept Program. Stifel, Nicolaus & Co.

The Alameda County Transportation Commission, California, (/AAA/AAA/) is set to price Wednesday $125.210 million of Measure BB limited tax senior sales tax revenue bonds, Series 2022, serials 2023-2041, term 2045. Citigroup Global Markets.

The Village Community Development District No. 14, Florida, is set to price next week $122.890 million of special assessment revenue bonds, Series 2022, terms 2027, 2032, 2037, 2042 and 2053. Jefferies.

The Barbers Hill Independent School District, Texas, (Aaa/AAA//) is set to price Wednesday $112.500 million of unlimited tax school building bonds, Series 2022, insured by Permanent School Fund Guarantee Program. Piper Sandler & Co.

The Nebraska Investment Finance Authority (/AA+//) is set to price Wednesday $106.980 million of non-AMT social single-family housing revenue bonds, 2022 Series D. J.P. Morgan Securities.

Competitive:

Denton, Texas, is set to sell $70.760 million of general obligation refunding and improvement bonds, Series 2022, at 11:15 a.m. eastern Tuesday.

Denton, Texas, is set to sell $110.360 million of certificates of obligation, Series 2022, at 10:45 a.m. Tuesday.

Seattle, Washington, (Aa2/AA//) is set to sell $263.825 million of municipal light and power improvement and refunding revenue bonds, Series 2022, at 10:45 a.m. Tuesday.

The Scott County School District Finance Corp., Kentucky, is set to sell $105.445 of school building revenue bonds, Series of 2022, at 11 a.m. eastern Wednesday.

The Clark County School District, Nevada, (A1/A+//) is set to sell $200 million of general obligation limited tax building bonds, Series 2022A, at 11:30 a.m. Wednesday.

Montgomery County, Pennsylvania, (Aaa///) is set to sell $155.220 million of general obligation bonds, Series of 2022, at 11 a.m. Wednesday.

Pueblo County, Colorado, is set to sell $126.355 million of Jail Project certificates of participation, Series 2022A, at 12 p.m. eastern Thursday.

The North Dakota Public Finance Authority is set to sell $320.800 million of taxable legacy fund infrastructure program bonds, Series 2022, at 10 a.m. Thursday.