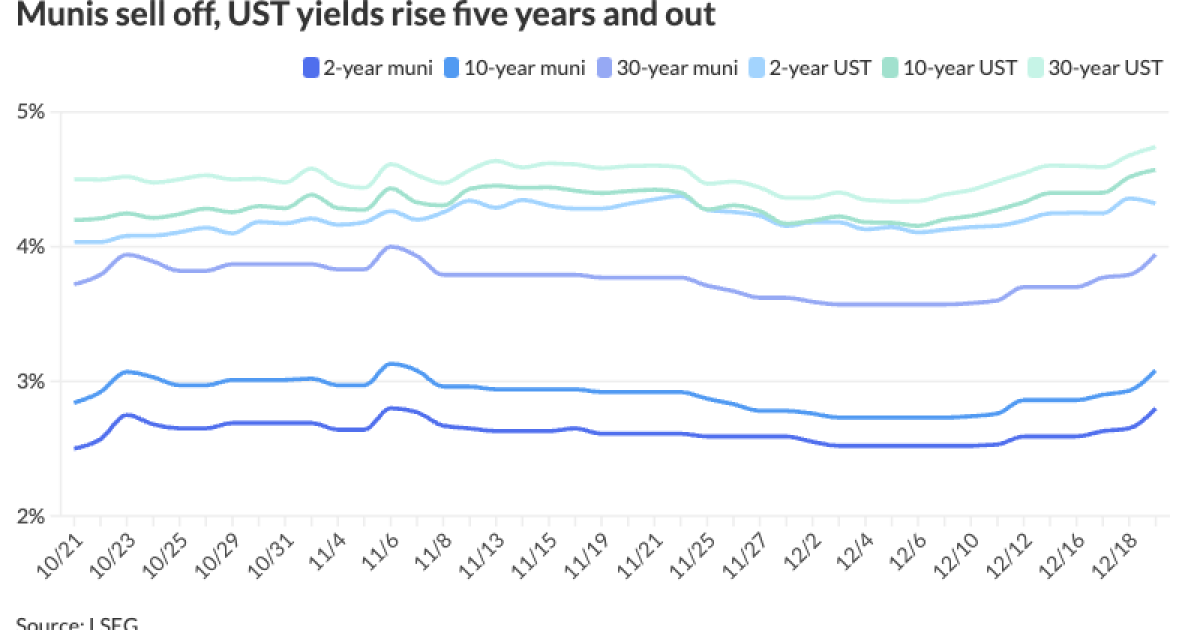

Municipals sold off Thursday, playing catch up to the U.S. Treasury’s extended rout across most of the curve. Equities ended mixed as all markets further digested macroeconomic uncertainty and

Muni yields rose 12 to 19 basis points, depending on the scale, while UST yields rose up to seven basis points out long.

Ratios rose as a result. The two-year municipal to UST ratio Thursday was at 65%, the five-year at 65%, the 10-year at 68% and the 30-year at 83%, according to Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 67%, the five-year at 66%, the 10-year at 69% and the 30-year at 84% at 4 p.m.

“Munis are grappling with a storm of uncertainty,” said James Pruskowski, chief investment officer at 16Rock Asset Management.

“Policy proposals from the new administration blur the line between talk and action,

Retail investors have taken note of the volatility as municipal bond mutual funds saw more outflows. LSEG Lipper reported investors pulled $857.1 million for the week ending Dec. 18, following $316.2 million of outflows the previous week.

High-yield municipal bond funds also saw outflows of $68.7 million compared to $192.3 million of inflows the previous week.

“With thin supply until late January and a strong reinvestment period, the stage is set for a compelling opportunity,” Pruskowski said.

The weakness came on the heels of the significant selloff in the market Wednesday, with stocks sharply lower and UST yields and the dollar significantly higher following the Federal Open Market Committee meeting, said JoAnne Bianco, a partner and senior investment strategist at BondBloxx Investment Management.

As expected, the Fed cut rates 25 basis points, but the Fed Chair Jerome Powell’s post-meeting comments about the “remarkable strength of the U.S. economy and the bright outlook probably made many market participants wonder why [the Fed] cut rates at all,” she said.

Over the last week and a half, the 10-year UST has risen over 40 basis points, Bianco noted.

Some of the changes made in the FOMC statement indicate the Fed may be starting to realize that inflation may not be tamed, she noted.

“So in their Summary of Economic Projections, the Fed increases its estimate for PCE inflation to 2.5% from 2.1% and they said that this measure won’t get down to 2% until 2027,” Bianco said.

Next year will see a new presidential administration, and there’s the potential for tax cuts, tariffs and deregulation, she said.

“All of these things pointing to the view that that the economy is going to remain strong next year, and investors will have a lot of opportunities in financial assets, including fixed income, in terms of the higher yields,” Bianco said.

Yields will be higher for longer, but that presents an opportunity for investors, she said.

“A reconciliation will occur of where near-term rates are headed following FOMC communications related to 2025 actions,” said Kim Olsan, senior fixed income portfolio manager at NewSquare Capital.

Tax-exempts will see some supportive factors, but some metrics may be signaling the development of further adjustments, she said.

Munis “have the benefit of a supply reprieve for a few weeks, which should help secondary bidsides,” she said.

Implied net demand in the next 30 days stands at negative $11.9 billion, with dealers taking some comfort in that figure, Olsan said.

However, dealers should also be mindful that issuance could “build early” in 2025, especially “if rates hold at the upper range and issuers sense market timing becomes more relevant,” she said.

Over the last 10 years, January issuance has averaged $27 billion, “which could prove constructive if next month’s supply does come in near that level as redemptions total about $20 billion,” Olsan said.

“The credit curve has rewarded higher-yielding issues this year, but a more tentative tone could bring wider spreads in the single-A, BBB and below-BBB ranges,” she said.

High-yield mutual fund inflows have been a “consistent draw” in the wake of rate volatility, Olsan said.

However, following the reaction of the Federal Open Market Committee meeting, “sub-investment grade trades pointed to wider levels,” she said.

A sale of Ba3/NR Houston TX Airport (subject to AMT) 5.25 s due 2033 printed at 4.53%, spread +161/BVAL, which was nine basis points wide to a late November sale at a yield of 4.39%, Olsan said.

With the pullback occurring this month, high-yield munis lost 1.10%, “lagging the broad market by 15 basis points and the AA-rated index by 22 basis points,” she said.

With rate uncertainty, flows can frequently “increase up” in credit as buyers seek safety and liquidity, she said.

With December’s total issuance never reaching an outsized figure — supply month-to-date stands at $30.16 billion — tax-exempt yields outperformed their taxable counterparts, though there may be further adjustments to come, Olsan said.

Since the first rate hike in March 2022, she said the 10-year AAA BVAL yield has “traded to a median -126 basis points against the 10-year UST.”

“The current spread is -156 basis points, for a gap of 30 basis points of implied ‘richness’ to the UST yield,” she said.

“A move toward a normalization of the AAA/UST relationship would place the 10-year AAA yield in the 3.25% vicinity, which last occurred in November 2023,” Olsan said.

Respective taxable equivalent yields would increase to around 5.50%, with longer-dated bonds surpassing 4.00% and generating TEYs above 6.50%, she said.

CUSIP requests fall

The aggregate total of identifier requests for new municipal securities — including municipal bonds, long-term and short-term notes, and commercial paper — fell 30.4% versus October totals. On a year-over-year basis, overall municipal volumes are up 10.0%.

Texas led state-level municipal request volume with a total of 177 new CUSIP requests in November, followed by New York (75) and Indiana (63).

There was a drop of 33.5% month-over-month for municipal bond identifier requests, but these requests are still up 9.3% year-over-year.

AAA scales

MMD’s scale was cut 15 basis points: The one-year was at 2.86% (+15) and 2.80% (+15) in two years. The five-year was at 2.87% (+15), the 10-year at 3.08% (+15) and the 30-year at 3.94% (+15) at 3 p.m.

The ICE AAA yield curve was cut 14 to 20 basis points: 2.99% (+20) in 2025 and 2.90% (+18) in 2026. The five-year was at 2.91% (+15), the 10-year was at 3.11% (+14) and the 30-year was at 3.91% (+14) at 4 p.m.

The S&P Global Market Intelligence municipal curve was cut 12 to 19 basis points: The one-year was at 2.88% (+12) in 2025 and 2.81% (+15) in 2026. The five-year was at 2.87% (+15), the 10-year was at 3.09% (+19) and the 30-year yield was at 3.89% (+17) at 4 p.m.

Bloomberg BVAL was cut 14 to 19 basis points: 2.95% (+15) in 2025 and 2.80% (+15) in 2026. The five-year at 2.88% (+15), the 10-year at 3.12% (+14) and the 30-year at 3.83% (+15) at 4 p.m.

Treasuries were weaker five years and out.

The two-year UST was yielding 4.320% (-4), the three-year was at 4.345% (-1), the five-year at 4.429% (+3), the 10-year at 4.571% (+6), the 20-year at 4.834% (+6) and the 30-year at 4.742% (+7) at the close.